Ignore the Headlines - Follow an Investment Strategy

Retirement Index InvestingA recent front-page headline from the October 6, 2017 Wall Street Journal (WSJ) made me think about investment related headlines from the last year. The headlines represent a sample similar to what you might see spanning decades of investing. The headlines continue to demonstrate that it is difficult to predict what will happen with markets in the short term, but everyone sure has their opinion.

Headlines can invoke fear or greed which may cause irrational action (following the latest hot trend) or inaction (staying in cash). I recall a conversation I had with someone around Christmas 2016. The individual moved all of their 401(k) investments into cash just before the 2016 November election. I am not sure what they have done since, but this is a good example of what can happen.

The Headlines

The October Wall Street Journal headline I refer to stated “Stocks Extend Record Run, Investors Wonder How It Ends?” The article sums up the past year with “Stocks continue their steady march higher, notching milestones not seen in more than 20 years, yet many investors see few obstacles to the seemingly endless run. ” and “That isn’t what many analysts and investors expected coming into this year, when they thought bond yields would rise as the economy heated up, and stocks would stall as valuations remained stretched.” You can follow the headlines from the last year to see how this played out over time.

Back in November, 2016 a WSJ headline “The Trump Trade Is Getting Out of Hand: Buy Bonds” proposed caution about the stock market.

But then in December, 2016 another WSJ headline declared “The Trump Trade: Stocks’ Biggest Post-election Rally Ever.” We ushered in 2017 with a January headline declaring that a “New Era for Rates, Regulation Dawns for Investors.”

By February the WSJ said “Investors Are Rethinking the Trump Trade” already. In April, the WSJ continued with “Investors Rethinking Risk – Rising unease fuels market turnaround after soft economic data, global conflicts.” And the New York Times let us know investors were thinking “Hitting a Speed Bump – The Trump bump took stock prices higher, but the market’s stalled. What’s next?”

As summer progressed to fall, The WSJ wondered in August “Are Stock Prices Too High? It Depends On How You Look at It.” Then in September we heard that “Dow Deja Vu: ‘Trump Trade’ Regains Favor” and “Stocks Won't Stampede With the Bulls Forever.”

What Can You Do?

It is challenging and confusing trying to make sense of the headlines and figure out how to invest. I suggest that you need to follow an investment strategy so that you can ignore the headlines and prevent yourself from making irrational decisions.

I personally subscribe to a long term investment strategy using low cost index funds where possible. The idea is to benefit from the growth and earnings of companies located throughout the world along with interest generated by corporate and government bonds. You determine the appropriate percentage of stocks you should own based on your investment time horizon, risk tolerance, investing experience, and purpose of the investments.

You can further break down your investment strategy by determining what percentage of your investments should be domestic and international and how often you want to re-balance your holdings. You may also need to adjust the type of bonds you hold based on your income tax bracket. Once you have your strategy set, then you simply follow the strategy and forget about the headlines.

Accumulation Investment Strategy

You might be wondering how to implement such a strategy if you still are saving and investing towards a long-term goal like retirement. Maybe you just started a new job and read the headline “Will You Be Ready When the Stock Market Crashes Again ?” On top of it, your fitness coach just told you they went to cash yesterday. What do you do?

To keeps things simple, consider an investment portfolio made up equally of two funds – The Vanguard Total World Stock Index Fund and the Vanguard Total Bond Market Index Fund held in a 401(k) plan. This sample portfolio is for demonstration purposes only and does not apply to every individual situation.

Your investment strategy could involve establishing monthly contributions to the 401(k) so that 50% of each contribution goes to the Total World Stock Fund and 50% goes to the Total Bond Fund. If your 401(k) plan provides the ability to re-balance, you could request a re-balance twice a year. Otherwise, you could set a calendar reminder to manually re-balance your account.

The scheduled re-balancing helps keep your portfolio on track so it doesn’t take on too much risk. For example, let us say that after six months you now hold 65% in the Total World Stock Fund and 35% in the Total Bond Fund. You now are exposed to more risk than you originally desired. A scheduled re-balance puts you back at 50% each. You did not have to try and digest all of the news headlines and figure out which ones might be right. You simply followed your strategy.

Likewise, if the opposite occurs and you now only have 35% in the Total World Stock Fund, you are now taking on too little risk. Following your strategy forces you to do something that is very difficult but necessary for long term wealth. You are buying stocks when they are on sale because you will be selling some of the Total Bond Fund and buying some the Total World Stock Fund that has dropped in value.

Retirement Investment Strategy

Once you are retired and living off of your investment portfolio, it becomes more challenging to ignore the headlines. The emotions surrounding your investments typically become a bit more intense. Ignoring the headlines becomes even more important at this time because you are using your portfolio to provide cash flow for your life!

Let us continue to use our very simple two fund investment strategy split equally between the Total World Stock and Total Bond funds. We’ll assume that you have figured out the annual dollar amount needed from your investments to support retirement.

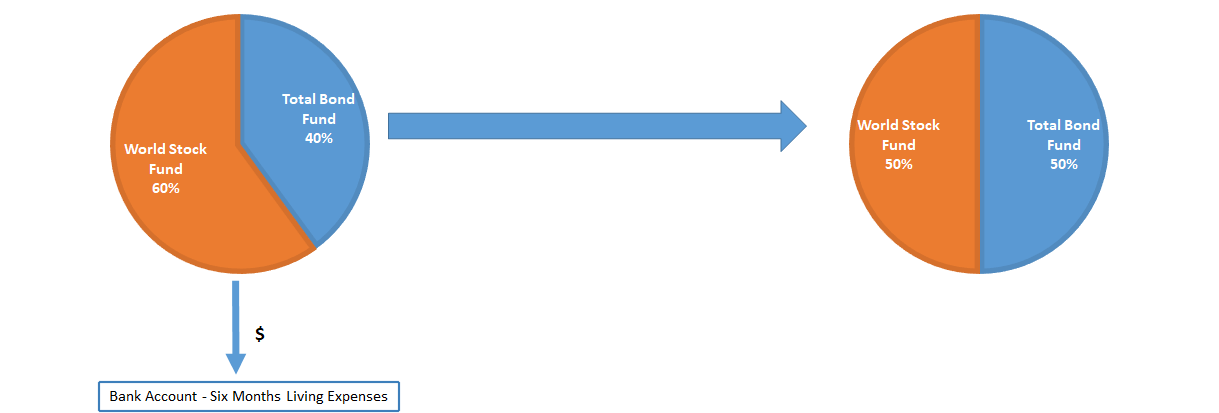

You retire with your funds held in a Traditional IRA and link the IRA to your local bank. Your portfolio starts out perfectly at 50% stocks and 50% bonds. You choose to let all dividends go to your IRA sweep or trading account. You have six months living expenses held in cash with your local bank.

Six months elapse and your bank cash reserves are running low. It is time to move another six months’ worth of living expenses from the Traditional IRA to your bank. Maybe a recent headline said “Investors Are Rethinking the Trump Trade” and you think now what?

It doesn’t matter. You simply look at how much cash you accumulated via dividends in the IRA over the last six months. This is your starting point. You sell some of one or both funds to generate the rest of the cash you need for the next six months.

How do you know what to sell. Again, you simply follow your strategy. For example, maybe the Total World Stock Fund is now 47% of your portfolio and the Total Bond Fund is 53% because of recent market behavior. You sell 3% of your bonds to generate the remaining cash you need which also brings you back to a 50/50 balance without worrying about the headlines.

Other scenarios of course could occur. Your ratio might already be 50/50. Then you would sell equal amounts of each fund. Or, stocks could have been on a tear and the Total World Stock Fund is now at 60%. You then sell approximately 10% of your stocks, transfer some cash to your bank, and reinvest the rest into the bond fund to achieve your desired balance.

In Conclusion

Notice that in both scenarios I didn’t say a thing about reading newspapers, magazine or blogs to figure out what to do with your investments. You simply follow your investment strategy whether you are retired or not. You ignore the daily noise and enjoy your life. This is not to say that you should not revisit your strategy over time.

The investment strategy that makes sense for a 25 year old single person starting their career will change as they are now married and nearing retirement. You may also develop a more robust strategy with additional bond diversification, additional investments like REIT index funds, and additional retirement cash reserves. The key is to avoid acting irrationally based on the latest headlines. You may also consider seeking professional financial help to make sure you have a sound strategy and serve as your sounding board while helping you ignore the headlines.

This content is developed from sources believed to be providing accurate information. The information in this material is not intended as investment, tax, or legal advice. It may not be used for the purpose of avoiding any federal tax penalties. Please consult legal or tax professionals for specific information regarding your individual situation. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.